The Retirement Threat Most People Overlook

And How You Can Protect Yourself

by Mike Marion

Published at LifeHealthPro.com

How important is it that your money lasts for the duration of your retirement? Most people would answer that it is the essential consideration. Yet, few people are aware of one of the most severe threats to a secure retirement.

The Problem

Sequence-of-Returns risk involves the order in which investment returns occur. In the accumulation (saving) stage, the investor can recover from a few bad years with a few good years later on. The situation is quite different during the period in which one is no longer working and saving, relying solely on investments for income.

If the first couple years of retirement happen to land within a declining market, the retiree may have no choice but to sell into losses. This depletes the principal they are depending on to grow within their retirement accounts. It is quite possible that the portfolio may never recover. This would result in either the retiree running out of money or having their lifestyle reduced from what they had planned on.

The bad news is that there is nothing an investor/retiree can do to control the timing of the market’s ups and downs. The good news is that retirement income planning tools exist that can mitigate this threat.

A Solution

To address the Sequence-of-Returns risk, a retiree should have a pool of money apart from their investments from which to draw income. A cash value life insurance policy is an example of such a source. This allows the retiree to withdraw income from the insurance policy instead of selling investment assets in a down market. The retiree can leave their regular retirement funds untouched so they can recover as the market moves back up.

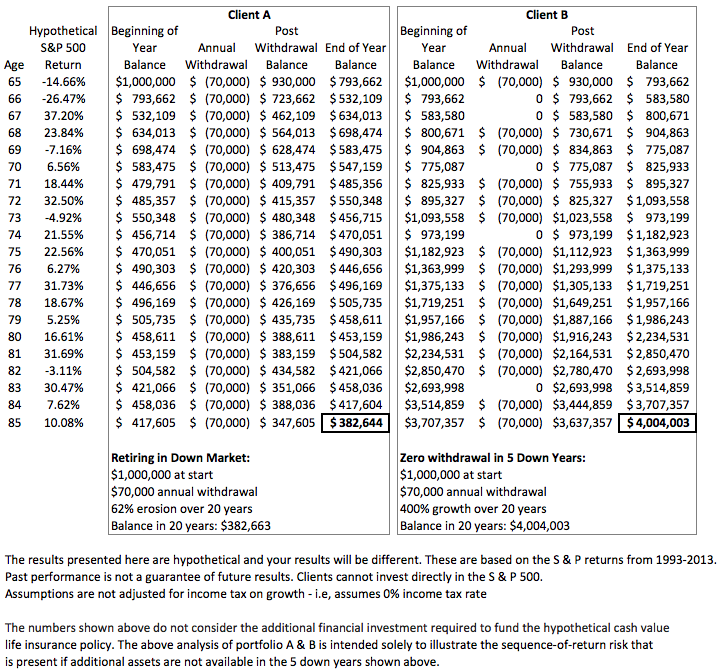

Consider the difference between the hypothetical scenarios of Client A and Client B. Both clients retire with $1,000,000 in the same year. Although they experience the same market returns, the balance of their portfolios after 20 years is vastly different. Client A withdraws $70,000 each year, including years with down markets. Client B also withdraws $70,000 per year, except for five years when the market was down, during which he leaves the $70,000 invested and instead withdraws it from the cash value of his life insurance policy.

At age 85, Client A has a balance of $382,644, while client B has $4,004,003 – over ten times as much! (see Exhibit A)

In this example, the normal benefits of life insurance will also still be in place. The insured’s loved ones will be protected with the policy’s death benefit and the insured will own an asset with special tax treatment.

For an individual who is still in their working years and is concerned about what might happen in the event that the market declines during or just prior to retirement age, cash value life insurance could be an important retirement income planning solution.

Exhibit A:

Mike Marion is the Director of Marketing at Marion Consulting, LLC and is a contributing author to LifeHealthPro.com. See his archive here.